At the moment, I am involved in some big sales projects for the (intermodal) logistics market, 4PL and construction offshore / projects. I noticed that within companies the question arises about assigning costs to activities, the revenues and determining the EBIT (Earnings Before Interest and Taxes). What are the costs of the activities and how well are they operating? What is our return on invested capital per process and activity? Where, when and how can we manage the processes and activities in an optimal way? Activity Based Costing lead to logistics ROI.

Because of my experience build over the years, this was not a surprise at all. This issue is of all times and places. What is different than before: due to the extensively available data of recent years, this issue is easier to manage. Most of the ‘old school’ ERP and company software have not been able to process and manage this challenge in a decent way. This means that the used software should be ‘ABC ready’ The advantages of ABC lead to logistics ROI.

Still, the knowledge of companies itself is leading and IT will provide you with the needed, arithmetical support.

What does the logistics management want to accomplish?

I would like to mention a concrete example. Containers will be distributed from (for example) Rotterdam to the Hinterland in Europe and most of the time through Germany. A lot of activities can be identified, like the transport of containers per barge, truck or rail. Temporary storage in a depot. Pre- and post-transport to the depot, the used transport modes and the locations.

In logistics, there is a high variety of activities, costs, additional costs and special tariffs. Besides, a lot of parties are involved in the supply chain.

Choices must be made. This is hard and, most of the time, there are a lot of alternatives. The financial flows are significant. Logistics management wants to realize an optimized process. In logistics, the ROI is under pressure for quite some years now! It is immediately needed as well!

Companies want to have the maximum ROI.

Multiple aspects have their influence. There are a lot of issues which can influence the ROI. The aspect regarding to planning is out of scope here. Advanced Planning & Scheduling (APS) is a subject itself. In this blog, the Activity Based Costing (ABC) is being discussed.

Activity Based Costing: what is it?

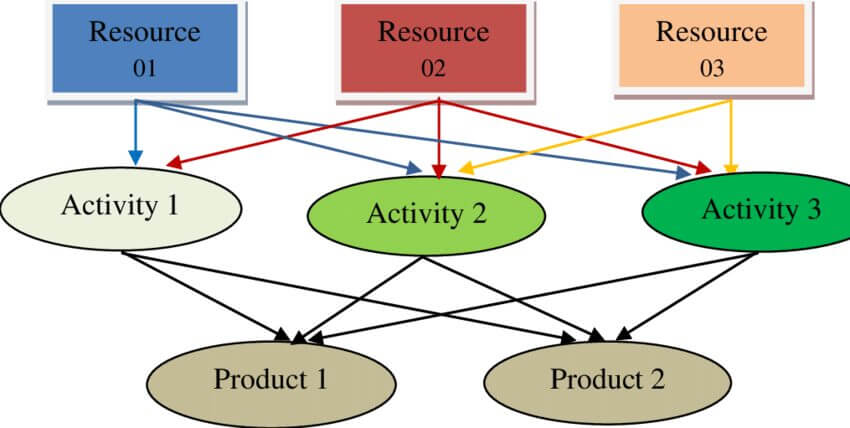

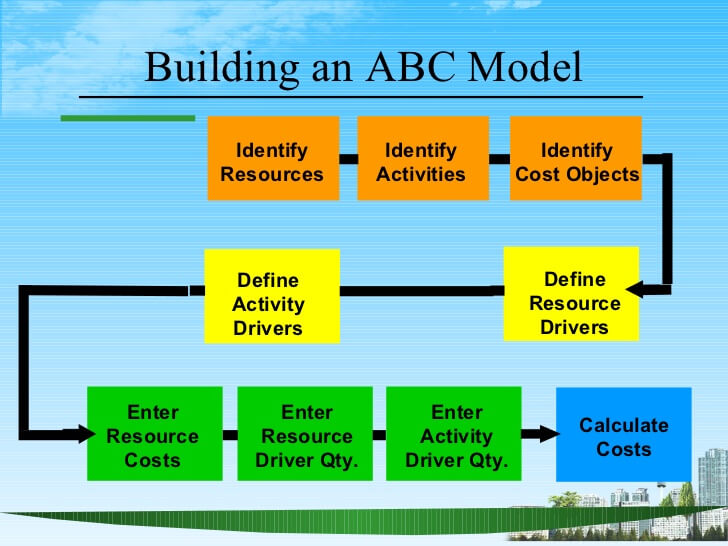

According to Dr. Dick van Damme, Amsterdam University, Activity Based Costing is very applicable to specify the indirect and overhead costs. In ABC, the costs are not assigned directly to cost units, like products, services or customers, but via an intermediate link: the activities. By specifying the costs per activity and after that assigning the activities to cost units, a detailed and accurate view on the actual costs of cost units is created. A list of the amount of activities required for the cost units can be identified per product, service or customer. By just summing up the costs per activity, you can easily find the total costs per cost unit.

When all six steps are done, the ABC-concept gives insight in the actual costs of a product, service or customer. This can give some surprising insights. A customer or product that generates quite a lot of revenue can cause that much costs that it can be useful to reconsider leaving the customer or take that certain product out of use.

I advise you to read this very interesting article by clicking on this link.

Introducing Activity Based Costing

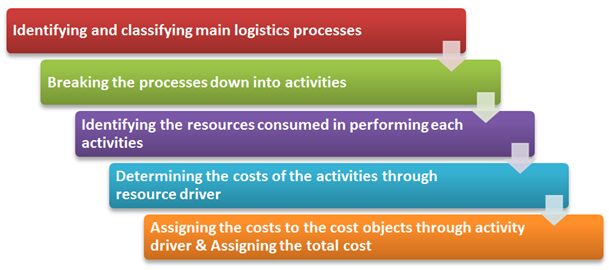

Activity Based Costing is a good method for calculating the total costs of a product of service. However, it is not suitable for every company. In order to introduce this method, accuracy is of utmost importance. According to WEKA, the following steps should be taken:

- Inform the employees and managers about Activity Based Costing. This will prevent uncertainties about the new system and rumours about reorganizations which could be the effect of ABC.

- Determine and describe the cost-centres (purchasing, logistics and administration).

- Determine the cost drivers (for example, quotations, transport costs and register invoices).

- Assign costs to activities and determine the price per activity.

- Determine to what extent every product uses the above-mentioned cost-centres and cost drivers.

- Determine the total costs per product. In other words: the total costs of an activity during a certain period to produce a product of service.

- Please read the entire article of WEKA by clicking on this link.

To be able to design and describe processes is of utmost importance.

To improve processes from a situation that you do not even control is not the smartest move to make. To optimize activities, it is important to gain insight in the content and performances of a process.

Process control will provide this insight. It is important to know that process control is a daily activity for all persons involved. It is about responsibilities, openness and standardization.

Process control leads to control of processes and activities and in that way control of the organization, the quality and the costs.

Author is Harry Luijk – Logistics & Supply Chain Professional and Partner at Merlyn Consult.